From Interface to Infrastructure: Where European Fintech Capital Is Flowing Next – 0100 Weekly Brief

Hello there,

European fintech’s identity crisis is becoming much more visible.

For more than a decade, Europe’s fintech boom was built around a relatively simple idea: build a better digital bank. Faster onboarding, simple interfaces, lower fees, and mobile-first experiences helped companies change consumer expectations around banking.

For this week’s brief, we looked across the latest developments involving Revolut, Monzo, fintech infrastructure providers, and emerging fintech ecosystems to understand how Europe’s fintech market is evolving beyond the neobank era.

The End Of The “Better Bank App” Era

For years, fintech competition centered around user experience.

Banking products were often slow, fragmented, and difficult to use. Neobanks simplified onboarding, introduced mobile experiences, and made financial services feel significantly easier to access.

Real-time notifications, card controls, spending analytics, and clean mobile interfaces became the defining features of Europe’s fintech wave. Now, they are industry standards. Financial products are becoming embedded inside broader workflows that combine payments, accounting, credit, cash management, and operational processes into a single layer.

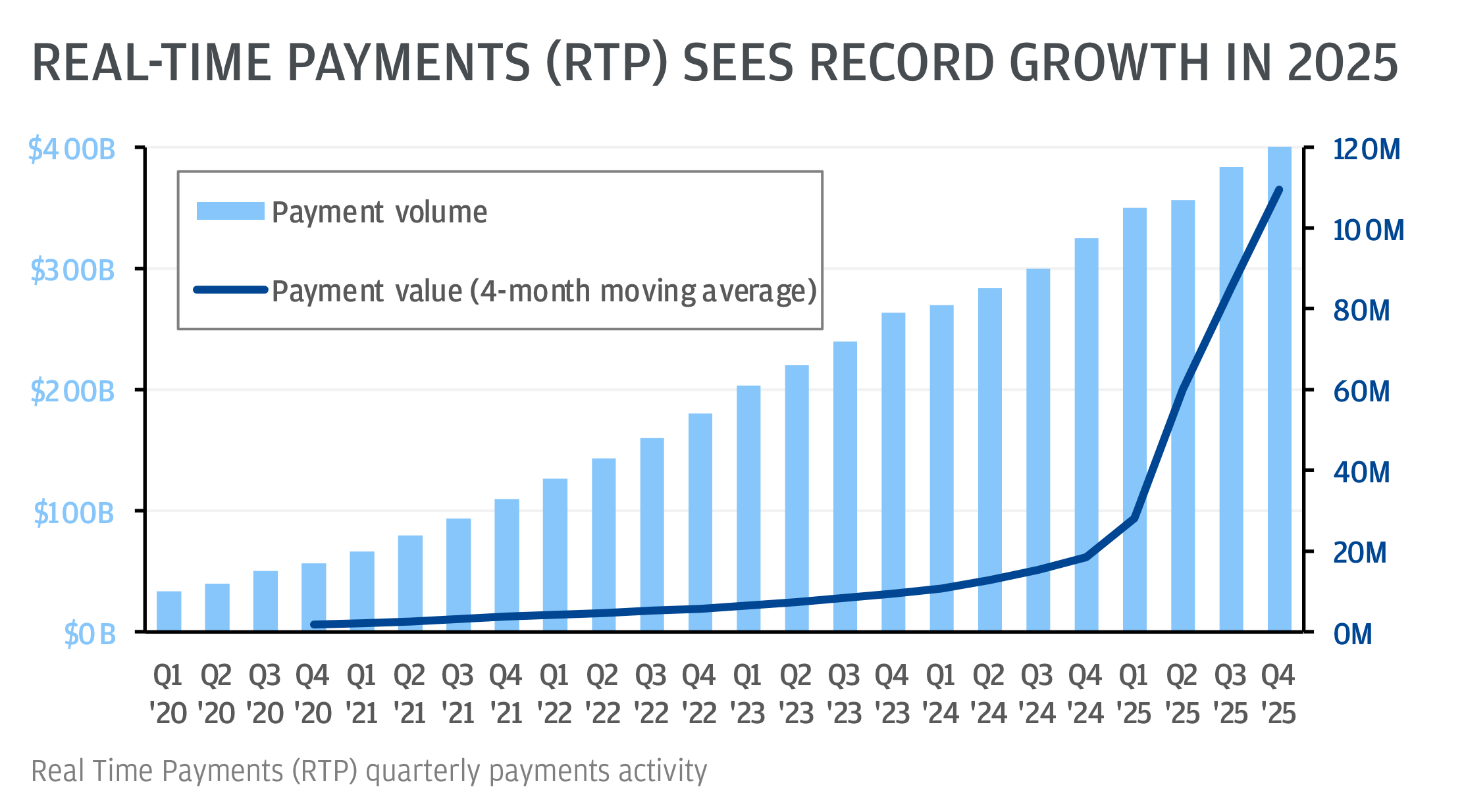

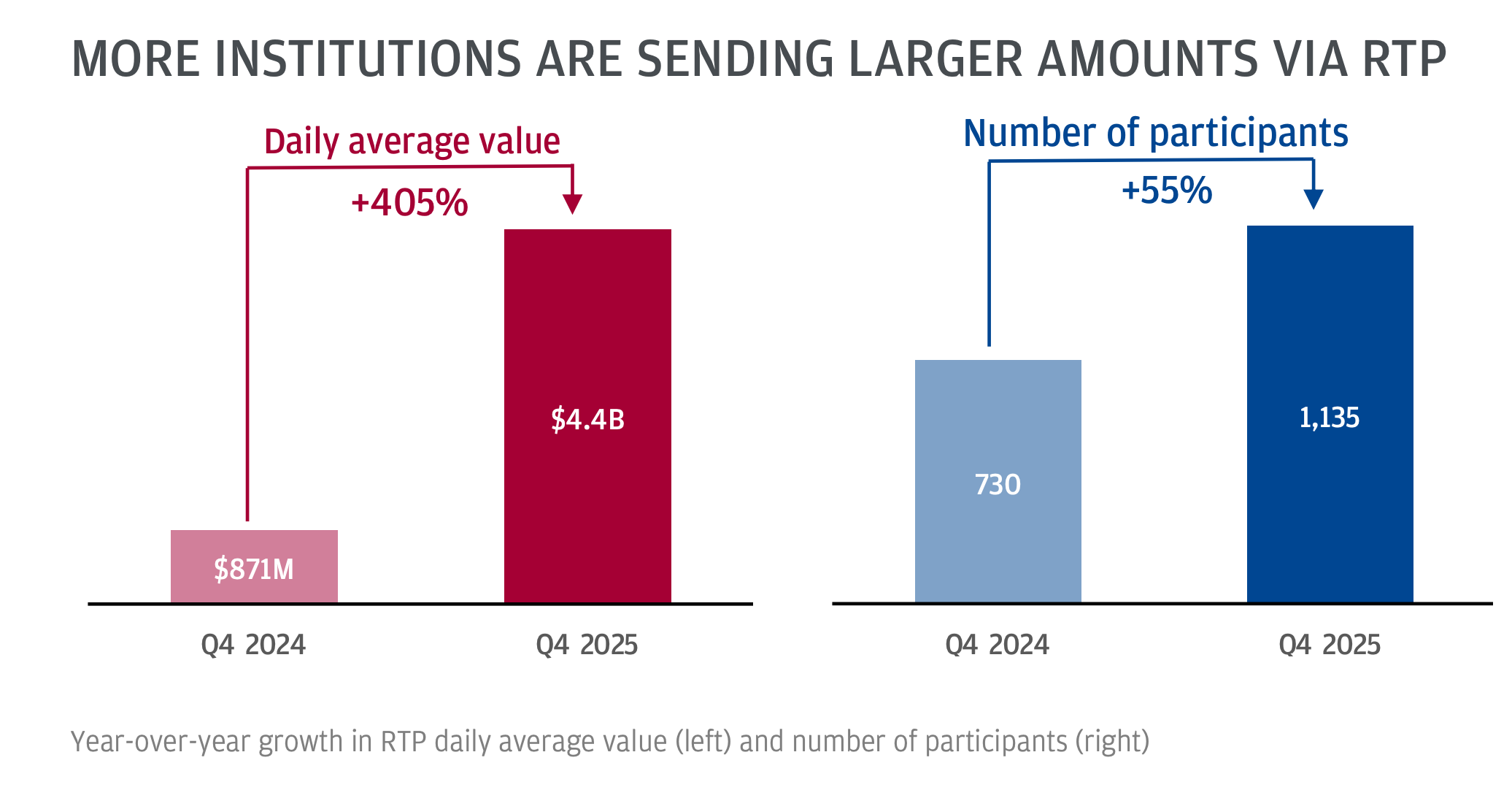

The market appears to be changing from interface innovation toward infrastructure innovation. The speed of money movement itself is becoming part of the product experience. According to JPMorgan data, daily real-time payment value increased by 405% year-over-year, while the number of participating institutions grew by 55% during the same period.

Consumers and businesses expect financial transactions to move as fast as information itself. Instant settlement is slowly moving from a premium feature to a baseline expectation.

According to Wamo CEO Deniz Guven, the real problem businesses face is not user experience itself, but fragmentation across banking, payroll, invoicing, procurement, and cash management systems.

“The problem is fragmentation, rather than the actual user experience,”

When payments, accounting, treasury, and lending all sit within the same operating environment, the bank account itself becomes only one part of a much larger workflow.

This also changes how fintech companies think about AI.

The earlier generation of fintech AI products often focused on customer-facing chatbots layered onto existing systems. Step by step, however, AI is being integrated deeper into underwriting, compliance, risk analysis, and operational automation.

Infrastructure Becomes The Product

That same transition is also influencing fintech business models.

A growing number of fintechs are now turning the internal systems they originally built for themselves into standalone infrastructure businesses sold to other companies. Starling’s Engine platform, Monese’s XYB infrastructure arm, Bunq’s banking-as-a-service expansion, and Bitpanda Enterprise all reflect the same underlying trend, according to Sifted.

Consumer fintech remains highly competitive, customer acquisition remains expensive, and many neobanks still struggle to convert deposits and interchange revenue into durable long-term margins. Infrastructure businesses, by contrast, often offer longer contracts, lower churn, and higher-margin software revenue

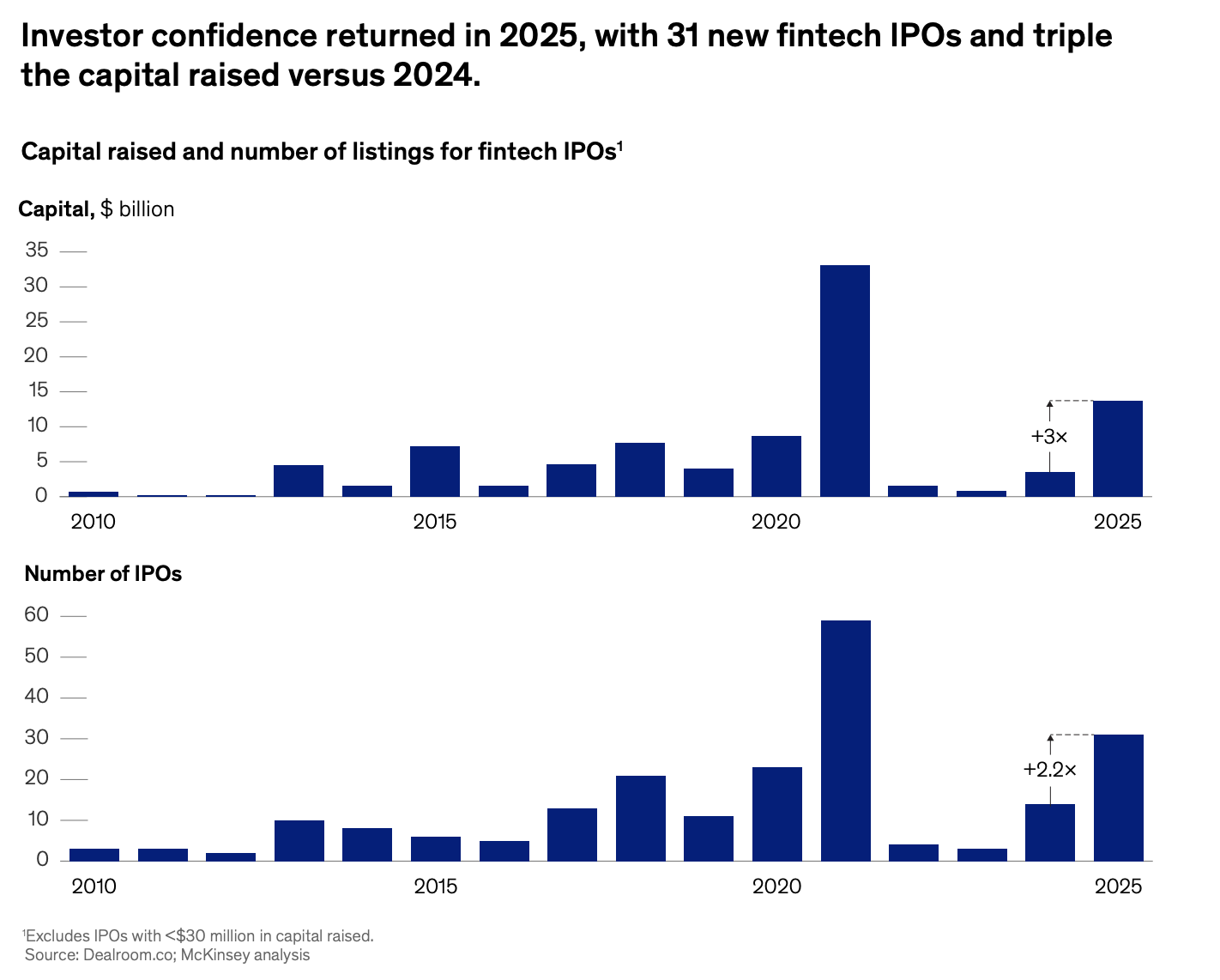

Investors appear to be rewarding that trend. Market data shows fintech’s share of total venture funding rose to 13.4% in early 2026 and remained above 10% for three consecutive quarters, while later-stage funding activity has steadily increased.

Rather than rewarding pure customer growth, capital is concentrating around companies with durable revenue models, stronger retention metrics, and infrastructure-like economics.

That dynamic is beginning to influence newer fintech companies from the beginning. Some startups are now launching consumer products partly as testing environments for infrastructure they eventually intend to commercialize more broadly.

Following the post-2021 environment, investors have also shown a preference for capital-efficient models with recurring revenues and long-term customer relationships rather than growth driven primarily by customer acquisition.

The numbers partly explain why. Embedded finance alone is expected to grow from roughly $45–58 billion in Europe into a market exceeding $400 billion over the next decade. In other words, the consumer app becomes both a distribution channel and a proof-of-concept layer for infrastructure.

Fintech’s earlier growth phase was largely built around customer acquisition. Its next phase appears to be about owning the rails underneath the customer experience.

The Next Phase of European Fintech

A few recent developments across Europe’s largest fintech companies are slowly starting to look less like startups and more like financial institutions.

Monzo has continued to expand beyond the UK following the acquisition of a European banking license, while simultaneously growing profits and diversifying revenue streams beyond traditional banking. Their latest annual results showed revenues rose 39% to £1.7bn, with four business lines each generating more than £300m in revenue: current accounts, borrowing, payments, and wealth. Business banking customers grew 45% and now contribute 14% of revenue.

Revolut is preparing to launch private banking services for customers with at least £500k to deposit, while also expanding into leveraged products, portfolio management, and wealth services.

Besides this, there is a “new bets” division that operates almost like an internal venture studio, funding experimental product ideas and scaling those showing strong early traction. In 2025 alone, Revolut reportedly generated more than £100m in revenue from 11 separate business lines.

Earlier generations of fintech models relied heavily on interchange fees, FX spreads, and deposit growth. But those revenue streams alone are often cyclical and difficult to scale sustainably.

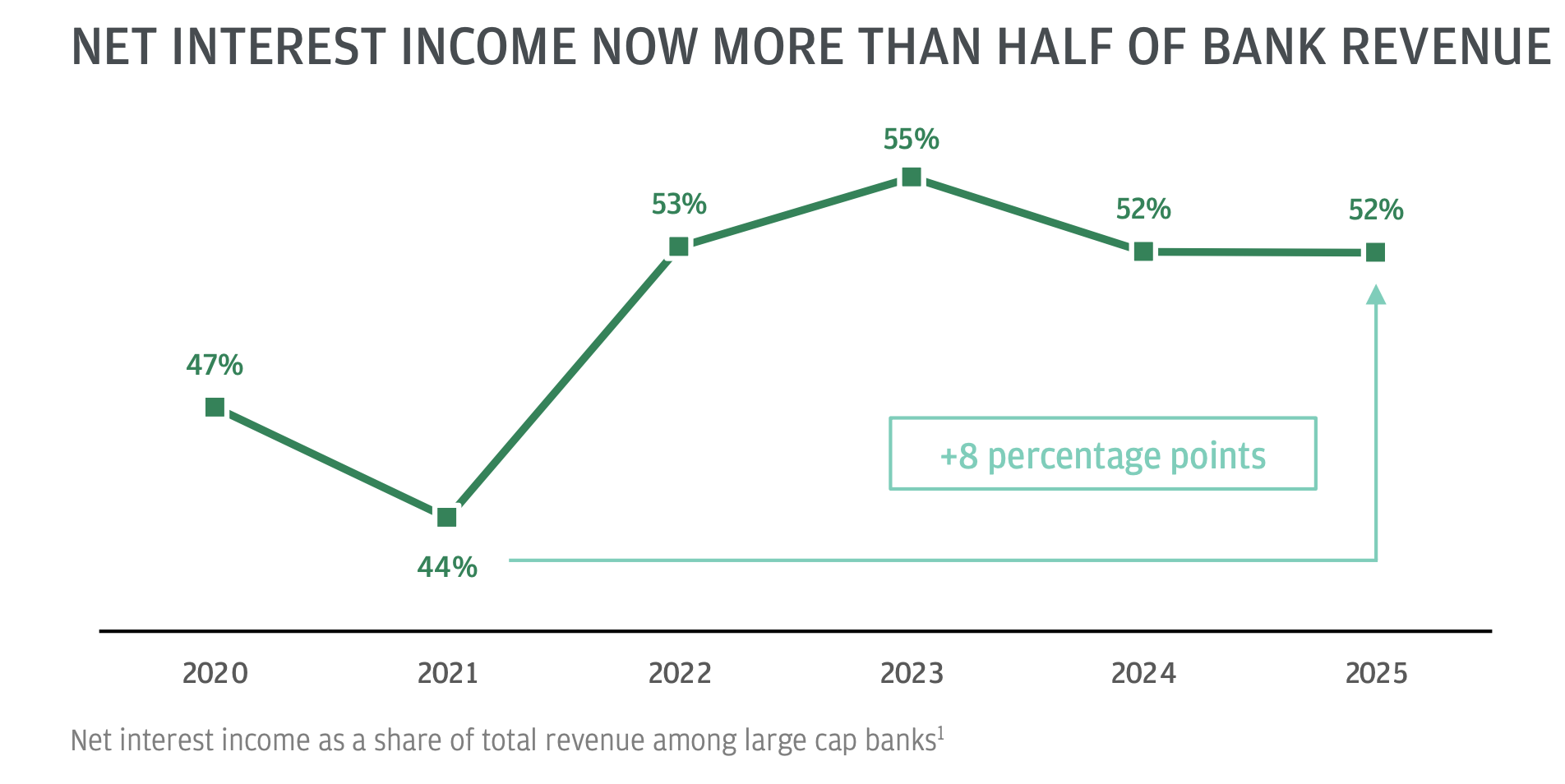

Higher interest rates have also accelerated another shift: fintech companies resemble financial institutions themselves. JPMorgan data shows net interest income now accounts for more than half of large banks’ revenue, while bank charter applications in 2025 exceeded the prior three years combined.

The distinction between fintech platforms and traditional banks is becoming difficult to separate. The larger European fintechs are now building multi-product ecosystems designed to increase wallet share across banking, lending, subscriptions, wealth, payroll, infrastructure, and enterprise services.

The Investors Backing the Next Layer

As European fintech shifts from consumer interfaces toward infrastructure, the investor landscape is shifting with it. The funds now writing the most consequential cheques are not simply chasing user growth — they are betting on the rails, the compliance layers, and the AI systems being built beneath the customer experience.

The Fintech Specialists

A handful of funds are built entirely around financial services and bring operational depth that generalist VCs rarely match.

QED Investors, founded by former Capital One executives and managing over $3B in AUM, has become the reference firm for infrastructure-oriented fintech. Their thesis centers on credit, regulated B2B infrastructure, underwriting, and payments, exactly the stack that the next generation of European fintechs is building on. Their portfolio includes Nubank, Klarna, Credit Karma, and Remitly.

Ribbit Capital takes a conviction-led approach across consumer and enterprise financial services, with a focus on payments infrastructure and embedded finance at Series B and beyond. They backed Revolut early and remain one of the most influential voices on where the market is heading.

Anthemis Group, based in London, operates at the intersection of fintech and systemic change, backing companies in embedded finance, InsurTech, and financial infrastructure with a portfolio spanning both Europe and global markets.

Portage Ventures brings a specialist lens with global reach, particularly active in backing B2B financial infrastructure companies that are expanding across Europe and emerging markets.

The European Generalists With Deep Fintech Conviction

Beyond the specialists, several European multi-sector funds have built genuine fintech expertise through early bets on the continent’s biggest breakout companies.

Index Ventures (London/San Francisco) is arguably the most influential European fund in fintech by portfolio quality, early investors in Revolut, Wise, and Robinhood, with deep pattern recognition across payments, neobanking, and financial infrastructure.

Accel’s London office has been consistently active across European fintech and B2B payments, combining early-stage conviction with the global network to help companies scale across markets.

Balderton Capital remains one of the most active early-stage backers of European fintech and SaaS, with a portfolio that reflects the shift toward infrastructure and recurring revenue models.

Lakestar has backed both Revolut and Stripe and continues to invest at the intersection of consumer fintech and financial infrastructure across Europe.

HV Capital (Munich/Berlin) closed its Fund IX at €710M and maintains a strong focus on fintech and climate tech across European growth-stage companies.

The Global Platforms

At the growth and late stage, the major US multi-sector platforms have become unavoidable participants in any significant fintech round. Andreessen Horowitz has backed over 10 fintech unicorns, including Stripe, Coinbase, and Brex, and has deepened its fintech practice consistently through 2025. Sequoia holds arguably the strongest fintech portfolio by outcome — Stripe, Nubank, Klarna, and Block, making it the most active investor by unicorn count in the sector.

What They Are All Watching

Across both specialists and generalists, investment activity is converging around the same set of bets: AI-native financial infrastructure, embedded finance, B2B payments, stablecoin settlement, and RegTech. The companies emerging from the Revolut alumni network, building ledgers, compliance tooling, and procurement automation, are landing on the radar of exactly these funds. The next wave of European fintech may be less visible to consumers than the neobank era, but for investors, that is precisely the point.

AI Becomes Infrastructure

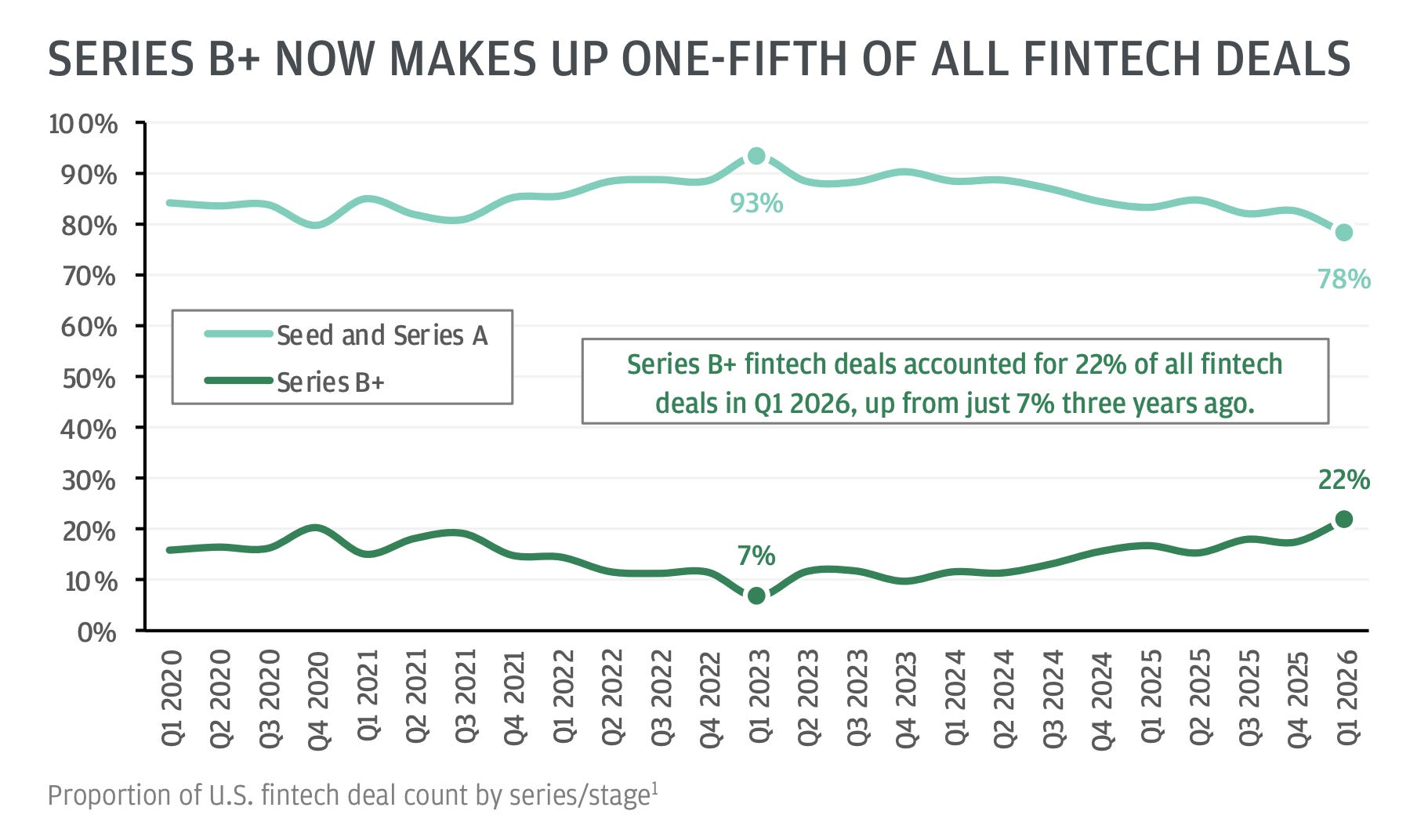

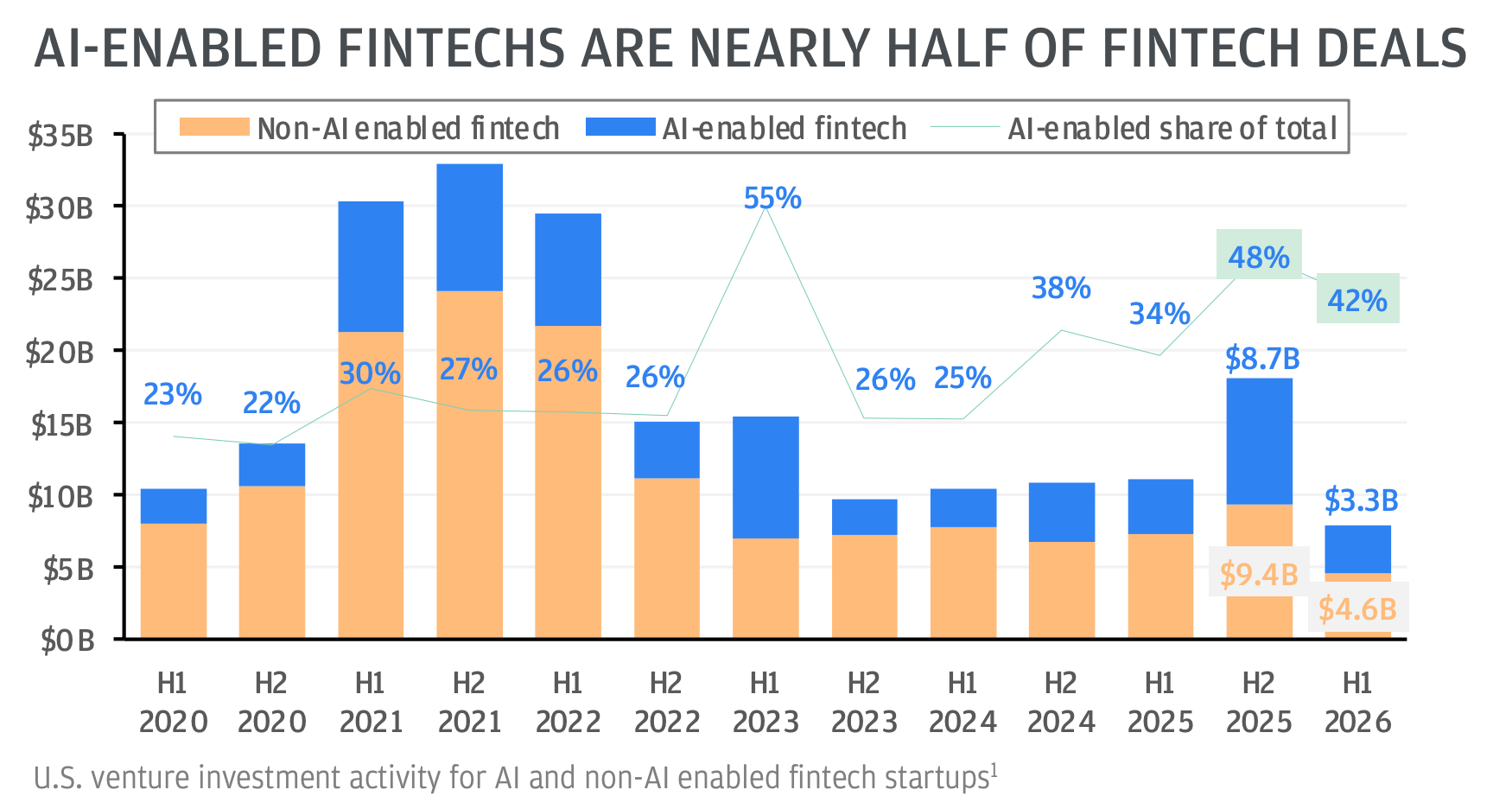

AI’s role inside fintech is also becoming much broader than customer-facing assistants. According to JPMorgan data, AI-enabled fintech companies now account for almost half of fintech deals, up from only 25% two years earlier. At later funding stages, AI-enabled fintech companies are also receiving significantly higher valuation premiums than non-AI peers.

Earlier fintech AI often focused on chat interfaces layered onto existing systems. So, AI appears to be moving toward underwriting, compliance monitoring, fraud detection, procurement, treasury management, and autonomous financial operations.

The change suggests AI may become less visible to customers while becoming important beneath the surface.

The Rise Of The Fintech Founder Factory

According to Accel and Dealroom data cited by Sifted, Revolut had already produced 46 entrepreneurs by March 2025. That number has likely grown further following the company’s secondary share sale, valuing Revolut at $75bn.

The startups emerging from the so-called “Revolut mafia” are also revealing where the market itself is moving. Many alumni are now building: payments infrastructure, stablecoin settlement systems, AI compliance tooling, banking ledgers, procurement automation, and biometric authentication systems.

Rather than recreating another neobank, many are building infrastructure and operational tooling for the financial system itself. The pattern resembles what happened previously in Silicon Valley with PayPal.

Private Markets In-Depth: The Future of Private Assets

Despite private markets being larger than public markets, access remains highly fragmented, involving intermediaries, registries, compliance layers, and operational processes that often create friction for both investors and companies. Weltix describes itself as an “operating system for private assets,” building digital infrastructure to manage onboarding, compliance, registration, custody, and, eventually, tokenization within a regulated framework.

What makes this particularly interesting within the broader fintech story is how closely it mirrors the evolution happening across banking. Earlier fintech cycles focused on creating better user experiences.

The next phase appears to revolve around owning the rails beneath the experience itself. Rather than simply digitizing access to investment, companies like Weltix are attempting to redesign how private capital moves through the system.