Private Credit Under the Microscope: Fear, AI Risk and the Institutional View – 0100 Weekly Brief

Hello there,

For years, private equity and private credit moved in parallel.

PE focused on ownership and upside. Credit focused on downside protection and yield. Different return profiles. Different teams. Different conversations with LPs.

In 2026, that separation is slowly fading.

Private credit is no longer just a capital solution sitting alongside buyouts. It’s impacting how deals get done, how portfolios are managed, and how exits are engineered. And if you’re in private equity, the change matters more than ever.

Why Private Credit Is Attractive for European Investors in 2026

Europe’s syndicated loan and high-yield bond markets remain smaller and less accessible than in the U.S., leaving a persistent funding gap for mid-market companies. Private credit funds have stepped into that gap with tailored, bespoke solutions and stronger lender protections, features that many allocators now see as a competitive advantage.

There is growing interest in private equity and private credit as LPs seek greater diversification, resilience, and access to high-quality assets outside traditional public markets.

said Stefano Zavattaro, Partner and Head of Italy at CAPZA

Mark Jochims, head of European Private Credit and a member of Morgan Stanley's Private Credit & Equity executive committee, also noted in a recent article the relative resilience of European private credit across economic cycles and its attractive risk-adjusted return profile. Floating-rate structures offer a natural hedge in a higher-for-longer interest-rate environment and conservative deal terms.

On the demand side, allocators themselves are vocal about the appeal. A recent panel of senior private capital professionals highlighted Europe’s less-crowded funding landscape and growing opportunity set as key reasons to increase allocations to Europe.

In practitioner circles, many echo this sentiment: market participants describe Europe as offering a “lender’s market” in certain mid-market segments, where disciplined underwriting can capture wider spreads and stronger covenants than in more mature U.S. markets.

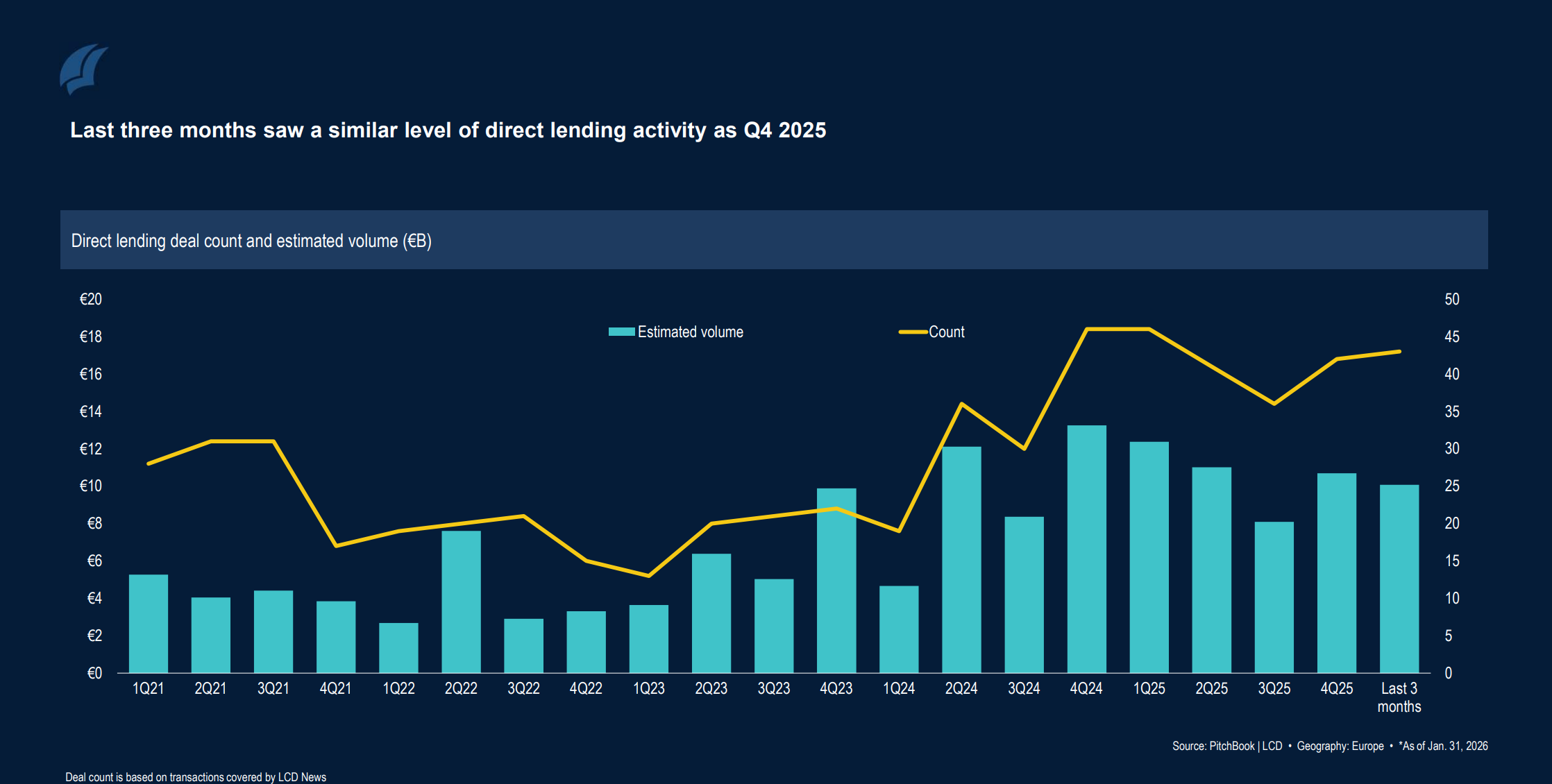

Direct Lending in 2026: Stable Activity & Better Structuring

The latest European data (as of January 31, 2026) show the deal count holding steady year-to-date, even as overall volume is slightly behind 2025. Over the last three months, activity has tracked closely with Q4 2025 levels, signaling stability rather than slowdown. Capital is clearly available, but underwriting is tighter, and lenders are being more selective about where they deploy it.

What stands out most is that acquisition financing is firmly back at the center of issuance. In January alone, 86% of direct lending loans supported M&A activity, totaling just over €2 billion in volume. LBO activity has been trending upward since the dip in Q3 2025, and in recent months, direct lenders have funded more than five times as many buyouts as the broadly syndicated market.

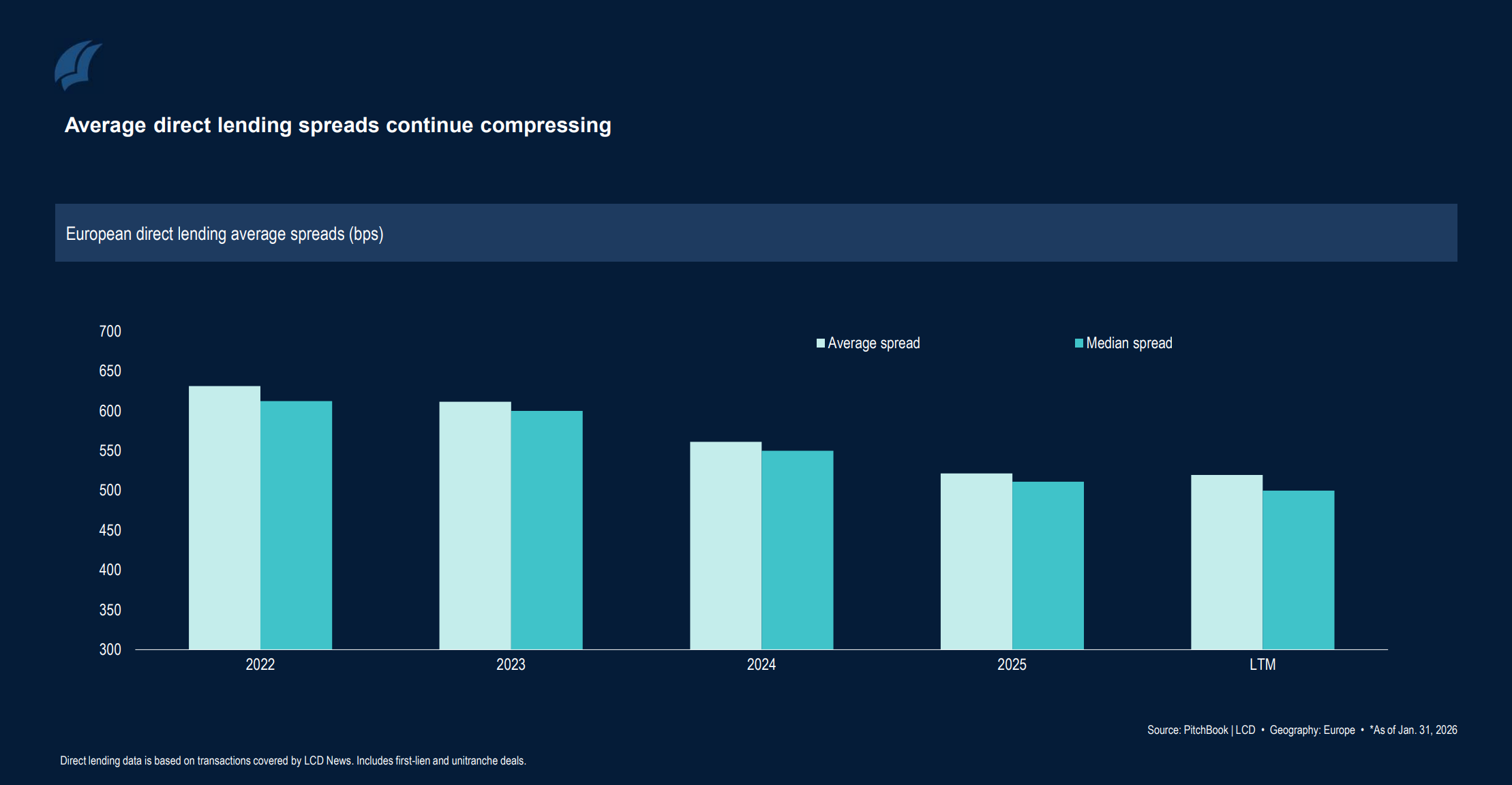

At the same time, spreads continue to compress. Over the past 12 months, average direct lending spreads have tightened to around 520 bps, with median spreads near 500 bps. Nearly half of the new LBO spreads have priced below 500 bps. Meanwhile, the leverage gap between BSL and direct lending markets has narrowed to less than one turn (0.7x), down from 1.31x in 2024. This reflects a mix of improving conditions in syndicated markets and a more measured approach from private credit funds as risk appetite moderates.

The Asset Class is Adapting To Slower Exist Dynamics

In 2025, firms completed a record $15 billion in continuation deals, up from about $4 billion the previous year. In these transactions, managers establish new funds to purchase loans from their older funds. This allows them to return some cash to investors while retaining assets that have not yet been repaid. Many of these loans were originally used to finance leveraged buyouts, but exits and refinancings have been delayed due to higher interest rates and weaker deal activity.

The increase in continuation vehicles reflects two clear trends: substantial capital raised in recent years and growing LP demand for distributions. While these structures can provide liquidity, they also extend the holding period of certain loans.

At the same time, investors are paying closer attention to credit quality, especially after several high-profile bankruptcies and concerns about how some funds may perform if higher rates continue.

What Is Investor Sentiment Saying About Private Credit?

Concerns around private credit have grown louder in recent weeks, particularly around AI disruption and credit quality.

Ares CEO Michael Arougheti described these fears as “odd” and “frustrating,” noting that 97% of the firm’s wealth clients have not requested redemptions and that institutional investors are not showing signs of panic. From his perspective, market volatility reflects sentiment rather than widespread distress, and underlying fundamentals in private credit remain stable.

Hamilton Lane’s co-CEO Erik Hirsch echoed that view, pushing back against claims of rising defaults and excessive leverage. Drawing on data spanning more than 68,000 private market funds and over 178,000 portfolio companies, he said defaults remain low and leverage levels broadly flat. Given Hamilton Lane advises on $860 billion in assets and manages $145 billion directly, Hirsch argues the firm has a broad vantage point across buyouts and private credit, and that the data does not support a narrative of systemic stress.

Still, skepticism is building in parts of the market.

An FT Alphaville analysis highlighted the concentration of private credit exposure in software and business services, particularly within Business Development Companies (BDCs), which represent roughly $450 billion of assets. UBS estimates that 25–35% of private credit portfolios face elevated AI disruption risk, with technology-heavy segments most exposed.

The debate now centers on whether private credit markets are accurately pricing disruption risk, or simply lagging equity signals. For now, industry leaders argue fundamentals are intact. But scrutiny around underwriting discipline and sector concentration is clearly increasing.

🗓️ 0100 DACH Panel Spotlight: Where LPs See Opportunity and Risk in PE

At 0100 DACH in Vienna, one of the key conversations will be the Fireside Chat: Where LPs See Opportunity and Risk in PE. As private equity enters a more selective cycle, LPs are reassessing where they want exposure—across small-, mid-, and large-cap strategies, geographies, and structures such as secondaries and continuation vehicles.

This session will examine how institutional investors are thinking about portfolio construction today, where they see the most compelling risk-adjusted returns, and how themes such as value creation and AI are influencing allocation decisions.

Bringing together Tanja Saaty (Managing Director at Constitution Capital), Jørgen Blystad (Investment Director at Argentum), and Bernhard Baumann (Managing Director, Private Markets at IW Group), the discussion will offer direct LP perspectives from fund-of-funds, institutional capital, and family office investors.

🌍 Across the Ecosystem | Thoughts on The Rising Interest in Private Credit

Institutional investors, insurers, pension funds, family offices, and private equity sponsors are increasingly aligned on the role private credit can play in portfolios: delivering stable income, structural downside protection, and greater control in volatile markets.

In a world where public fixed income has struggled to provide both yield and predictability, private credit is viewed not just as a complement to buyouts but also as a strategic allocation in its own right. Below is a snapshot of how the debate around private credit as a core allocation is evolving across the European private markets ecosystem, along with recent headlines from this area.

🗞️ News | Fortress’ Latest Private Debt Fund Seeks to Lure Insurance Firms

Fortress Investment Group is adjusting its latest private debt vehicle, Fortress Lending Fund V, to better attract insurance companies and European institutional investors. According to people familiar with the matter, the firm is adding an unleveraged sleeve to the fund, which will primarily focus on direct corporate loans. Previous vintages of the strategy offered only a leveraged version, so this new structure marks a shift to meet insurers’ capital and regulatory preferences.

By introducing an unleveraged option, Fortress is aligning the fund more closely with the needs of insurance balance sheets, which often favor lower-risk, capital-efficient structures. The move reflects broader demand from European insurers for private credit exposure that offers yield and downside protection without additional leverage risk, signaling how managers are tailoring products to capture growing institutional appetite in the asset class.

📄 Article | Private credit can ride out the tech storm

In a letter responding to the FT’s Lex column on the “SaaSpocalypse,” Nick Baldwin of Lincoln International argues that concerns about AI-driven disruption in software-heavy private equity portfolios may not translate into systemic risk for private credit.

He notes that for European private lenders, AI-related disruption has been a core underwriting consideration since late 2022. Rather than treating “software” as a single category, lenders distinguish between narrow tech solutions that face displacement risk and broader, AI-integrated platforms that may actually benefit from the change.

🗞️ News | CAPZA Raises Nearly 1.4 Billion Euros For Private Debt 7 Fund

CAPZA, the private debt arm of BNP Paribas Asset Management Alternatives, has completed the first closing of its CAPZA Private Debt 7 fund, raising nearly €1.4 billion. The amount already exceeds half of what was raised for its previous vehicle, CAPZA Private Debt 6, marking a significant milestone for the firm’s private debt platform. The strong early close reflects continued investor appetite for CAPZA’s strategy, which is backed by a 20-year track record in the asset class.

The fundraising drew support from both returning investors and new LPs, with more than 30% of commitments coming from international markets, including Germany, Belgium, Italy, Japan, and the Middle East. The broad geographic participation underscores CAPZA’s expanding global footprint and highlights sustained demand for European private credit strategies among institutional investors seeking stable income and diversification.